Last updated: May 2026

US businesses alone pay over USD 7 billion annually in IRS penalties related to payroll tax compliance errors and 40% of small to mid-size US businesses incur a payroll penalty every year (Rise Global Payroll Compliance Report, 2026).

For businesses operating across multiple countries simultaneously, the exposure compounds with every jurisdiction added. This guide covers eight strategies that finance and HR teams can apply right now to manage cross-border payroll tax compliance accurately and without costly gaps.

What Is Payroll Tax Compliance in Cross-Border Operations?

Payroll tax compliance means meeting every tax withholding, filing, reporting, and remittance obligation that applies to your employees in each country where they are based, not where your company is registered.

That distinction is critical. An employee working in Singapore is subject to Singapore’s CPF contribution rules, tax withholding requirements, and MOM filing deadlines regardless of whether their employer is incorporated in Australia, the US, or the UK. Each additional country your workforce operates in adds a new set of obligations.

Over 30 countries updated payroll, employment tax, or mandatory benefits rules between 2025 and 2026 (Deel Global Payroll Compliance Checklist, 2026). Regulatory velocity is not slowing down. The businesses that manage this well are the ones with deliberate systems and specialist support in place before problems arise.

What Are the Key Payroll Tax Risks in Cross-Border Operations?

Before covering strategies, the risk categories must be understood clearly. These are the four compliance failures that generate the most penalties in cross-border payroll:

| Risk Category | What It Means | Consequence |

|---|---|---|

| Worker misclassification | Treating an employee as a contractor under local law | Back taxes, penalties up to 10–50% of annual payroll in some jurisdictions, forced reclassification |

| Late or incorrect filings | Missing country-specific deadlines for tax remittance or reporting | In the US, a 10% IRS penalty applies for deposits made more than 15 days late (Global Wealth Protection, 2025); fines average USD 1,100 per employee per incident globally (Rise, 2026) |

| Permanent establishment (PE) risk | An employee’s sustained presence in a country triggers corporate tax obligations | Unexpected corporate tax liability in that jurisdiction, even without a registered entity |

| Double taxation | Employees taxed in both the home and host countries without treaty relief applied | Financial loss for the employee, reputational damage, and potential legal liability for the employer |

Critically, 42% of organisations have no formalised global payroll strategy at all, and a further 30% are still developing one (Rise, 2026). Operating without a documented strategy is a material business risk, not an administrative gap.

How Do You Ensure Payroll Tax Compliance Across Multiple Jurisdictions?

Strategy 1: Get Worker Classification Right in Every Country Before Hiring

Misclassification is the most common and most expensive cross-border compliance failure. What qualifies as an independent contractor relationship in one jurisdiction does not automatically qualify in another.

The EU Platform Work Directive in force since December 2024 and requiring full transposition by December 2026, establishes a legal presumption of employment for platform workers meeting defined control criteria across all 27 EU member states.

The US Department of Labor suspended its 2024 Independent Contractor Rule mid-year 2025, creating classification ambiguity for businesses that had already adapted (Rise, 2026). In Australia, the courts have continued to tighten the definition of employment in recent Fair Work decisions.

The correct approach is a classification review for every worker in every country before engagement begins, not after a query from a tax authority. Procloz’s contractor management service handles compliant classification, onboarding, and payment across 50+ countries.

Strategy 2: Build a Country-by-Country Compliance Calendar

Every jurisdiction has its own tax filing deadlines, social contribution schedules, and annual reporting requirements. Missing a deadline by a single day can trigger a penalty or spark a tax audit (Neeyamo, 2025).

A cross-border payroll compliance calendar must include, for each country:

- Payroll tax withholding deadlines (monthly, quarterly, or per pay cycle)

- Social security and statutory contribution filing dates

- Annual payroll reporting deadlines (P60, W-2, STP, IR8A, Form 16, and equivalents)

- Minimum wage review dates Indonesia raised provincial minimums by 5–7% from December 2025; the UK confirmed a further increase for April 2026 (Rise, 2026)

- Any mid-year legislative changes that affect calculations retroactively

Automated deadline tracking via a global payroll platform eliminates the manual monitoring burden. Procloz’s global payroll services include automated compliance deadline management across all active markets.

Strategy 3: Understand Tax Residency Rules for Every Employee

Tax residency is the foundation of cross-border payroll compliance. It determines how much tax to withhold, which forms to file, and which reporting obligations apply, and it is not simply about where an employee holds a passport.

Physical presence tests, domicile rules, and treaty tie-breaker provisions all affect tax residency determinations.

A remote employee working from a country different from where they are contracted may trigger tax obligations in two jurisdictions simultaneously. Even a single day of work in certain countries can trigger filing obligations for both the employee and the employer (GTN, 2025).

Shadow payroll arrangements, where a separate payroll is run in the host country alongside the home country payroll, are required in some jurisdictions for employees on international assignments.

This is a specialised compliance area that requires country-specific expertise rather than general payroll processing capability.

Procloz’s in-country expertise covers tax residency analysis and shadow payroll requirements across key markets, including Australia, Singapore, India, the Philippines, New Zealand, and the US.

Strategy 4: Apply Double Taxation Treaties Correctly

When employees or business operations span multiple countries, double taxation, being taxed on the same income by two governments, is a direct risk without active treaty management.

Tax treaties between countries define which jurisdiction has primary taxing rights over specific types of income.

The US-India tax treaty, for example, means business profits are typically only taxed in one country unless the company has a permanent establishment in the other.

Businesses must track which treaties apply to their employee locations, ensure treaty elections are filed where required, and document the basis for any treaty exemptions claimed.

Treaty positions must also be reviewed when employees move countries, when new markets are entered, or when a country renegotiates its treaty network.

Relying on assumptions from a prior year without checking for treaty changes is a common source of unexpected tax exposure.

Strategy 5: Implement Robust Payroll Systems Capable of Multi-Jurisdiction Processing

Manual payroll processing across multiple countries is not scalable and introduces material error risk at every step, including currency conversion, tax rate application, statutory deduction calculation, and filing deadline tracking, all of which require country-specific logic that spreadsheets cannot maintain reliably.

Cloud-based payroll platforms with built-in multi-jurisdiction compliance logic reduce this risk substantially. Key capabilities required for cross-border payroll:

| Capability | Why It Matters |

|---|---|

| Automated local tax calculations | Eliminates manual rate errors as tax tables update |

| Multi-currency payroll processing | Handles exchange rate application and currency-specific deductions |

| Real-time regulatory update feeds | Flags legislative changes as they occur, not at year-end |

| Integrated statutory filing | Generates country-specific payroll reports and files directly with tax authorities where available |

| Audit trail and record retention | Meets the multi-year record-keeping requirements of each jurisdiction |

| Role-based access controls | Protects sensitive payroll data across distributed teams |

Procloz’s global payroll services operate on a cloud-based, multi-jurisdiction platform covering all of these capabilities across 100+ countries.

Strategy 6: Conduct Regular Cross-Border Payroll Compliance Audits

Internal or external payroll audits are how businesses catch compliance gaps before tax authorities do. An audit that finds a problem costs significantly less than a regulatory audit that finds the same problem.

A cross-border payroll compliance audit should cover:

- Worker classification review for all contractors and employees in each country

- Verification that payroll calculations match current statutory rates, contribution rates, tax thresholds, and minimum wages, all of which change annually across APAC and beyond

- Reconciliation of payroll tax filings against actual payments made

- Review of employment contracts for compliance with current local law

- Confirmation that data protection obligations are being met per jurisdiction

Annual audits are the minimum viable frequency for multi-country operations. Quarterly reviews are appropriate for businesses operating in markets with great regulatory change velocity.

Singapore, Indonesia, Malaysia, and India all made material payroll-related changes in 2025 and 2026

Procloz’s workforce advisory and consulting service supports cross-border compliance audits and provides ongoing regulatory monitoring across all active markets.

Strategy 7: Manage Permanent Establishment Risk Proactively

Permanent establishment (PE) is a tax concept that most HR teams underestimate. When an employee works from a country, particularly in a sustained, structured way, their presence can trigger corporate tax obligations for the employer in that jurisdiction, even without a registered entity or office there.

The key PE triggers in most jurisdictions are:

- A fixed place of business, and an employee regularly working from home in a country can qualify

- Sustained presence exceeding the physical presence thresholds defined in the relevant tax treaty

- Authority to sign contracts on behalf of the company in a foreign country

- A dependent agent, an employee who habitually concludes contracts in a country, creates PE exposure

The correct mitigation is to assess PE risk for each remote employee’s country before the working arrangement begins, not after 12 months of undocumented presence. Using an Employer of Record means the EOR is the legal employer in that country, which significantly reduces direct PE exposure for the client company.

Strategy 8: Partner With In-Country Payroll and Tax Specialists

No single in-house team can maintain accurate, current knowledge of payroll tax law across 10+ jurisdictions simultaneously. Tax codes change, contribution rates are updated, and new reporting obligations are introduced, often mid-year and with short implementation timelines.

Partnering with specialists who operate in each country daily is the most reliable way to stay current. The right partner structure for cross-border payroll is an aggregated model:

a global payroll provider that coordinates a network of in-country specialists in each market, delivering consistent oversight at the global level with locally accurate compliance execution at the country level.

Procloz operates this model across 100+ countries, with dedicated in-country expertise teams covering employment law, payroll tax, and statutory compliance in each key market, including outsourced payroll services in Australia, payroll services in Singapore, and payroll services in the US.

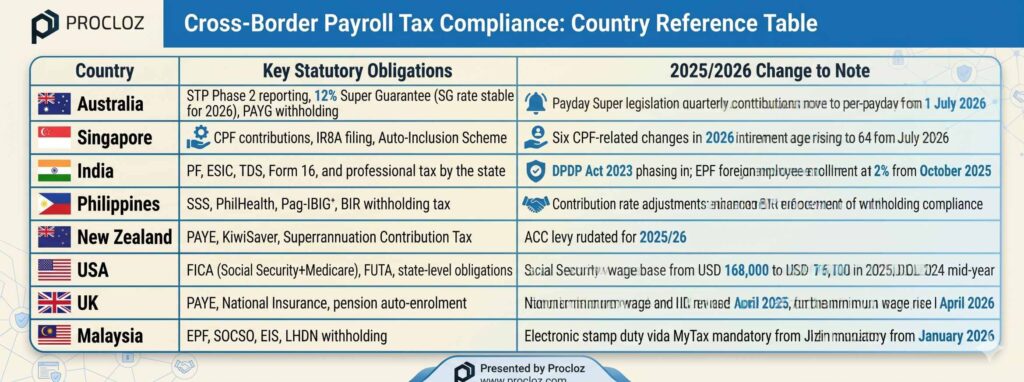

Cross-Border Payroll Tax Compliance: Country Reference Table

Frequently Asked Questions on Payroll Tax Compliance in Cross-Border Operations

What is the most common payroll tax compliance mistake in cross-border operations?

Worker misclassification engages workers as independent contractors when they meet the legal definition of employees under local law. This triggers backdated payroll tax liability, penalties, and mandatory benefit back-payments.

The EU Platform Work Directive, US DOL guidance changes, and tightened Australian Fair Work decisions have all raised the stakes in 2025 and 2026. Classification must be reviewed country by country before each engagement begins, not applied uniformly from the home market’s standards.

How do you avoid double taxation for employees working across multiple countries?

By identifying and applying the relevant tax treaty between the countries involved. Tax treaties define which country has primary taxing rights over specific income types. Where a treaty applies, the employer must ensure the correct treaty elections are filed and documented.

Shadow payroll arrangements are required in some jurisdictions for employees on international assignment. This is a specialised area general payroll software does not automatically apply treaty positions. Country-specific tax expertise is required for each affected employee’s situation.

When does an international employee create a permanent establishment risk for their employer?

When their presence in a country is sustained and structured enough to constitute a fixed place of business or to habitually conclude contracts on the company’s behalf. The specific threshold varies by country and by the relevant tax treaty.

Remote employees working from home in a foreign country can create PE risk even without a formal office. Using an Employer of Record significantly reduces direct PE exposure because the EOR, not the client company, is the legal employer in that country.